20 weeks until the arrival of Buy Now Pay Later (BNPL) regulation: What firms can expect

26 February 2026 | Written by Chris Warhurst

The “Buy Now, Pay Later” (BNPL) sector is currently facing its most significant shift since its creation, as interest‑free agreements under 12 months come under the Financial Conduct Authority’s (FCA) regulation for the first time.

When is this regulation arriving?

BNPL becomes fully regulated on 15 July 2026, marking a fundamental shift in how the sector operates. In the months ahead, firms must demonstrate readiness across affordability, disclosures, and customer support in line with the FCA’s expectations.

Key requirements include:

- Mandatory affordability checks for every transaction

- Reciprocal Data sharing to the credit reporting agencies (CRAs)

- Updated disclosure standards, aligned with Consumer Duty

- Enhanced missed‑payment communications to reduce complaint risk and improve customer outcomes

On 11 February 2026, the FCA published their final rules for Deferred Payment Credit (DFC), confirming that the interest‑free, short‑term BNPL product will fall under full FCA regulation from July this year.

What firms need to do

To succeed under the increased regulatory scrutiny, firms will need to demonstrate compliance without impacting the frictionless journey that consumers have come to expect – using evidence, consumer feedback and data‑driven testing over intuition.

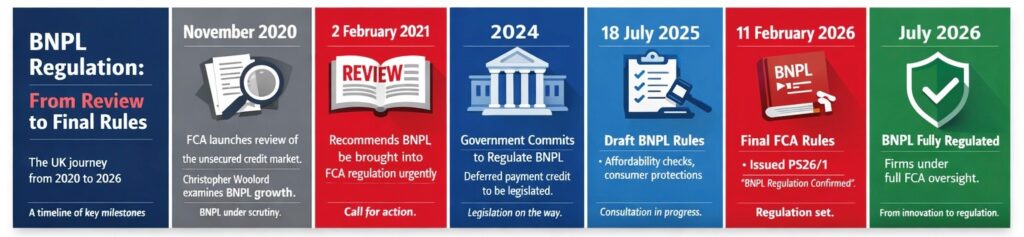

Many BNPL providers have been on this journey and preparing for the past 5 years since the Woolard review in 2020 with key milestones illustrated below.

Figure 1 – UK BNPL Regulation Timeline

Nature of the upcoming regulations

The focus of regulation should be on consumers, ensuring they are able to use BNPL to manage their credit payments and build their credit profiles, while also protecting them from unsustainable debt.

Therefore, one of the more immediate challenges facing BNPL firms is the introduction of mandatory creditworthiness and affordability requirements.

Affordability

The FCA is mandating creditworthiness assessments on every BNPL transaction. This brings BNPL into line with broader consumer‑credit expectations and gives lenders a responsibility that goes beyond simple checkout convenience. Affordability checks must be evidence based, proportionate to order value and in the case of high frequency digital shopping providers must be executed in under a second.

This will mean reliance on providers such as CRAs and other third parties who hold income and expenditure data to provide quick assessments and verification of their disposable income.

BNPL’s transition into mainstream credit reporting

Under the final rules, firms will have to inform consumers if they will obtain CRA data. In turn BNPL must share back consumer performance data with the CRA(s) they obtain data with under the rules of reciprocity.

This requirement is another key step in BNPL’s evolution into mainstream credit reporting. It raises the bar on:

- Data‑quality management

- Governance expectations around credit information

Furthermore, new remedies set out by the FCA’s Credit Information Market Study (CIMs) are expected to mandate that firms share data to all three of the UKs major bureaux (Experian, Transunion and Equifax) within the next couple of years.

BNPL reporting to credit bureaux covering both arrears and positive repayment behaviour creates a valuable new dataset for the broader credit market.

Consistent, timely repayments serve as a strong indicator of credit discipline. This is particularly beneficial for individuals who are new to the UK credit market, such as younger people or recent arrivals, allowing them to make small, regular purchases to gradually build their credit profile. Similarly, reported missed payments may highlight early warning signs of financial stress.

Mainstream lenders should look to leverage BNPL performance data to strengthen creditworthiness and affordability checks and early‑warning indicators across their portfolios.

CRA’s will need to continue to evolve and work hard to create real time data and analytical solutions that brings fairness to BNPL consumers. Ensuring regular up to date payers can improve their credit profile as well as protecting consumers from unsustainable debt.

FOS and missed payments

Missed‑payment handling is a critical area of consumer risk, and the FCA has tightened expectations here as well. Firms must provide clear communication when payments are missed, including appropriate signposting to debt‑advice organisations.

Poor execution in this area quickly drives up complaint volumes, and the financial consequences can escalate fast. At £650 per Financial Ombudsman Service (FOS) complaint, even a handful of cases can dwarf the value of an average £80 digital shopping BNPL transaction.

Additional guidance is expected next year on how the FCA may mitigate the FOS cost exposure for lower‑value credit products, including potential adjustments to case fees for low‑value products – something many BNPL lenders will be watching closely.

Section 75 protection

Section 75 of the Consumer Credit Act 1974 applies to items costing over £100 but not more than £30,000, as it does for credit cards currently. It means the BNPL provider will be jointly liable with the retailer if anything goes wrong.

Temporary permissions regime timeline

Firms without the required regulatory permissions by 15th May 2026 will enter the Temporary Permissions Regime (TPR).

TPR for BNPL is a regulatory framework that allows firms without the necessary consumer credit permissions to continue their DPC whilst their applications for full FCA authorisation are assessed. Under TPR, firms must still comply with the regulatory requirements whilst progressing with the authorisation process which must be within six months of Regulation Day.

The TPR includes a supervised run-off regime (SRO) for firms exiting without full authorisation allowing then to service existing agreements for up to two years.

BNPL market context

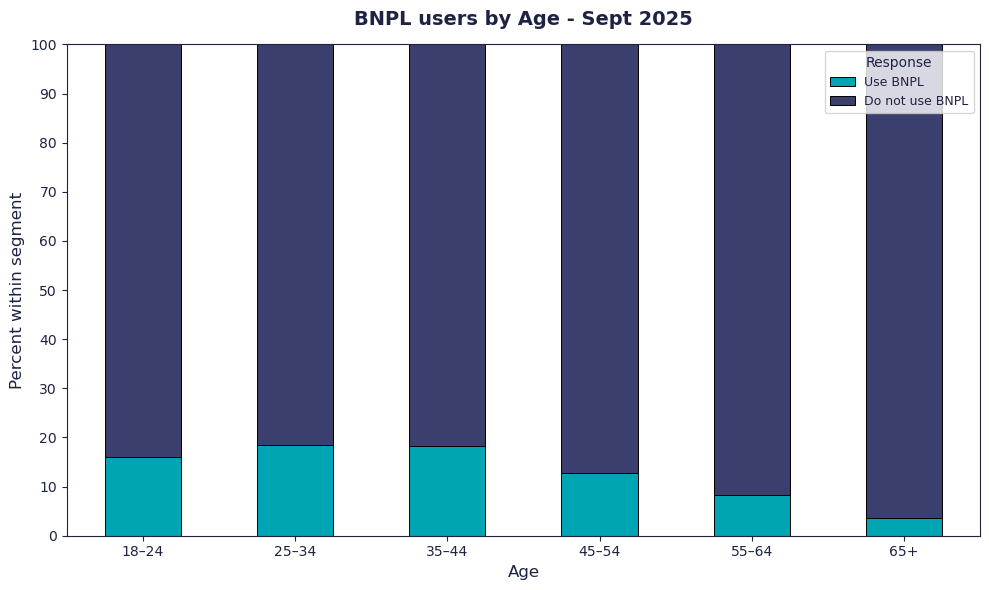

The need for regulation is underscored by the scale of the sector. According to the FCA, BNPL lending has grown from £0.06bn in 2017 to more than £13bn in 2024, with around 20% of UK adults using BNPL in the 12 months to May 2024. Popular for those aged 18 to 54 as illustrated from the graph using based data from the Bank of England.

Figure 2 – % BNPL users by age (Source: Bank of England / NMG Household Survey Research datasets | Bank of England)

The new framework seeks to preserve innovation while ensuring lending is responsible and sustainable for consumers across all income groups.

Other markets context

It’s helpful to consider international comparisons, particularly markets where BNPL adoption is also popular. The UAE, for example, introduced a structured BNPL regulatory framework in 2023, requiring licensing, affordability controls, and clearer consumer disclosures.

In the US, the regulatory picture has recently moved in the opposite direction, with the CFPB withdrawing key BNPL guidance and deprioritising enforcement of its BNPL regulation in 2025, signalling a retreat from tighter federal oversight.

Europe, by contrast, is moving firmly towards stronger regulation: the EU’s Consumer Credit Directive (CCD2) brings virtually all BNPL products in scope, mandating stricter affordability assessments, expanded disclosure requirements, and full credit-worthiness checks across the block.

Our view

Our view at 4most is that BNPL can offer an affordable and transparent way to manage costs and build a credit profile however we welcome the move to regulate the sectors to ensure lending is responsible.

We believe that early adoption of proportionate affordability assessments, implementing robust risk and fraud controls, alongside effective use of data, supports responsible lending practices.

Additionally, providing a clear and streamlined customer journey enables lenders to lend effectively and responsibly.

These measures in turn help to avoid the rising credit risk and fraud costs associated with the rapid expansion of the BNPL sector.

Robust data quality management is also at the heart of this to monitor and understand credit performance and ensure quality reporting to the CRAs.

We have seen that when lenders fail to implement these measures, they can struggle and ultimately withdraw from the market.

Want more guidance?

Send us an email if you would like to discuss how these upcoming regulations might impact your organisation – info@4-most.co.uk.

Authors

Interested in learning more?

Contact usInsights

Breaking down the impact of M&A on IFRS 17 reporting: A Comprehensive IFRS 17 Framework for Business Combinations

22 Apr 26 | Insurance

The Renters’ Rights Act: What 2026 holds for landlords’ costs and the impact on buy-to-let (BTL) affordability

09 Apr 26 | Banking