Managing IFRS 9 and Climate Risks

09 January 2024

Managing IFRS 9 and Climate Risks

As we move into the new year and new plans are made, one area that is in need of enhancement and rapidly gaining attention from regulatory bodies such as the Prudential Regulation Authority (PRA) and the European Banking Authority (EBA) is lender’s approach to incorporating climate risk into IFRS9 estimates.

In the UK, since the release of SS3/19, and in Europe with the release of the EBAs Actions Plan on Sustainable Finance [1], the requirements to start to understand the impacts of lending on climate change have been apparent. However, it is fair to say that addressing pressing issues such as the COVID19 pandemic and the cost-of-living crisis may have taken priority since 2020. In 2024, Regulator expectations are now that lenders should be making asserted efforts to ensure that climate change is considered appropriately within financial reporting.

In 2024 the PRA expects to see an “increasing use of quantitative analysis in climate risk assessments to support strategic decision making for financial reporting” [2]. The EBAs report on IFRS9 implementation by EU institutions (Nov 23) underlines “Institutions are expected to incorporate, when appropriate, model adjustments at the level of model parameters and to continue progressing towards the integration of climate and sustainability-related risks in ECL outputs” [3].

The world’s appreciation of, and engagement with, climate change has been beset with doubts, the perceived watering down of commitments made within COP 28 highlights this. The financial world is no different, with a longer-term horizon of impacts and wide range of assumptions leading to a range of uncertainty.

It is clear that regulatory bodies will not see uncertainty as an excuse for inactivity in this space. A movement in the right direction will both demonstrate a positive intent and inform further evolution of approach. Engaging with this subject earlier is likely to inform requirements for further data capture, modelling and management strategies which will require time to bear fruit.

In light of this 4most has been considering options and as with all challenges, there are a range of possible solutions. Scenario modifications, model enhancements, changing staging criteria or better informing judgemental overlays are varied ways to demonstrate that climate change is an important part of the process of estimating credit losses and informing business decisions.

As evident from published results and climate disclosures, lenders are at different stages of evolution with regards to their approach to this challenge. Cognisant that lenders range in size and complexity, 4most has the ability to deliver solutions appropriate to each organisation.

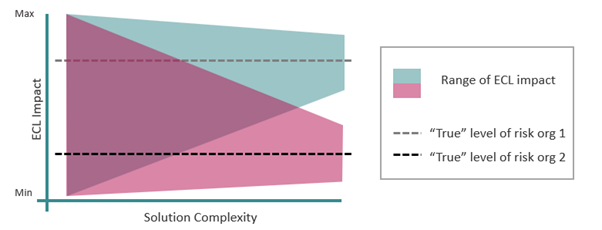

Incorporating climate risks into IFRS9 is likely to vary in terms of the impact on the Expected Credit Losses (ECLs) and more complex approaches are likely to present a narrower range of impacts closer to the “true” level of risk the organisation is exposed to (whether high or low).

Less complex or overly judgmental solutions are likely to add more conservatism or result in no (or very low) impact on ECL, which may or may not be appropriate. More considered solutions are likely to better reflect improvements in the understanding of both physical and transitional risks, whereas simpler approaches will be less responsive to the future evolution of this understanding.

The most important element is for lenders to demonstrate that climate risk has been appropriately considered within the reported ECL’s, recognition of weaknesses and that there is a vision for continued enhancement.

If you are looking at ways to incorporate climate change into your IFRS 9 process, please get in touch.

Interested in learning more?

Contact usInsights

Is your firm ready for the upcoming changes required for credit reference agency (CRA) reporting?

31 Mar 26 | Banking

Preparing for the Bank of England’s Second System-Wide Exploratory Scenario (SWES): Next steps for private credit firms

23 Mar 26 | Banking

20 weeks until the arrival of Buy Now Pay Later (BNPL) regulation: What firms can expect

26 Feb 26 | Banking

Ruya Bank partners with 4most to deliver IFRS 9 ECL framework and ongoing execution support

24 Feb 26 | Banking

4most named as a supplier on Crown Commercial Service’s Digital Outcomes Specialist 7 RM1043.9 framework

23 Feb 26 | Data