Is your firm ready for the upcoming changes required for credit reference agency (CRA) reporting?

31 March 2026 | Written by Veronika Papazova

With credit information market reform accelerating, firms reporting data to credit reference agencies (CRAs) must prepare for Financial Conduct Authority (FCA) led change.

On 25 February 2026, the FCA released consultation paper CP 26/7, in efforts to modernise the UK’s credit information landscape. This has the potential to significantly alter operations for CRAs and firms (both as data contributors and consumers of bureau products) resulting from mandated reporting across all three major CRAs and improved data quality and dispute handling.

CP 26/7 follows the FCA’s 2023 Final Report from the Credit Information Market Study (CIMS) launched in 2019 and signals a shift from diagnosing problems to implementing solutions as illustrated . Refer to our previous article on CIMS and why credit reporting matters from 2023.

Figure 1: Credit Information Market reform

What are the direct impacts for firms that are Data Contributors?

1 – Mandated reporting across all three major CRAs (Remedy 2A)

- Lenders will be mandated to share consumer credit agreement and performance information with all FCA designated CRAs (DCCRAs) if not doing so already (Experian, Equifax, TransUnion).

- If your firm is one of the 275 that currently provides to either one or two of the three designated CRAs you will be impacted by this change. While the initial technical impact of change has been minimised by the CRAs all accepting each other’s data formats along with the Standard Industry Reporting Format (SIRF) firms will still need to consider:

- Relevant data sharing agreements and contractual arrangements with each additional CRA will need to be put in place, and privacy notices updated where necessary.

- Anticipate & mitigate for the greater number of queries firms should expect in relation to the data they share – ensuring operational processes continue to be fit for purpose.

2 – Improved data quality and dispute handling (Remedy 2D)

- A more rigorous approach to data accuracy and error correction. The proposals introduce stronger responsibilities for firms that submit data, tighter processes for resolving consumer disputes, and more consistent reporting of satisfied CCJs and decrees. The goal is to reduce consumer harm caused by outdated or incorrect information and to give credit files greater integrity.

- As a result, firms will need to demonstrate robust operational processes for the handling of disputes and consumer queries – meeting this standard may require enhancements to its operating model and processes.

Implementation timeline

The FCA proposes a 12-month implementation period once the policy statement is published.

After which:

- Firms already reporting to a DCCRA must comply immediately at the end of the 12-month window.

- Firms reporting for the first time have an extra six months to onboard.

Given the scale of expected system changes, data quality uplift, and governance enhancements, firms should begin internal assessments now rather than waiting for final rules.

What does this mean for firms that consume bureau products?

Upcoming changes will result in greater consistency between the three designated CRAs with respect to the data they receive. However, differences in address matching, settings and a broader scope of data not captured by this change will mean that CRAs will continue to offer material differences in the aggregated data and credit scoring that they provide.

An observation of the 2022 CIMS Interim Report noted material discrepancies between the three CRAs, notably: “for individuals that have a default recorded with at least one of the CRAs, the 3 large CRAs hold consistent information on the number of defaults for only around 30% of them ” (FCA MS19/1.2 Credit Information Market Study Interim Report and Discussion Paper) – refer to Chapter 4).

The aim of remedies 2A and 2D will be to address this inconsistency, but differences observed in public data within the same analysis are perhaps early evidence that while these measures will improve alignment – particularly for defaults & arrears, differences are likely to remain.

The figure below and summary observations set out our expectation of how the FCA remedies covered by this Consultation Paper will impact aggregated credit data and scores:

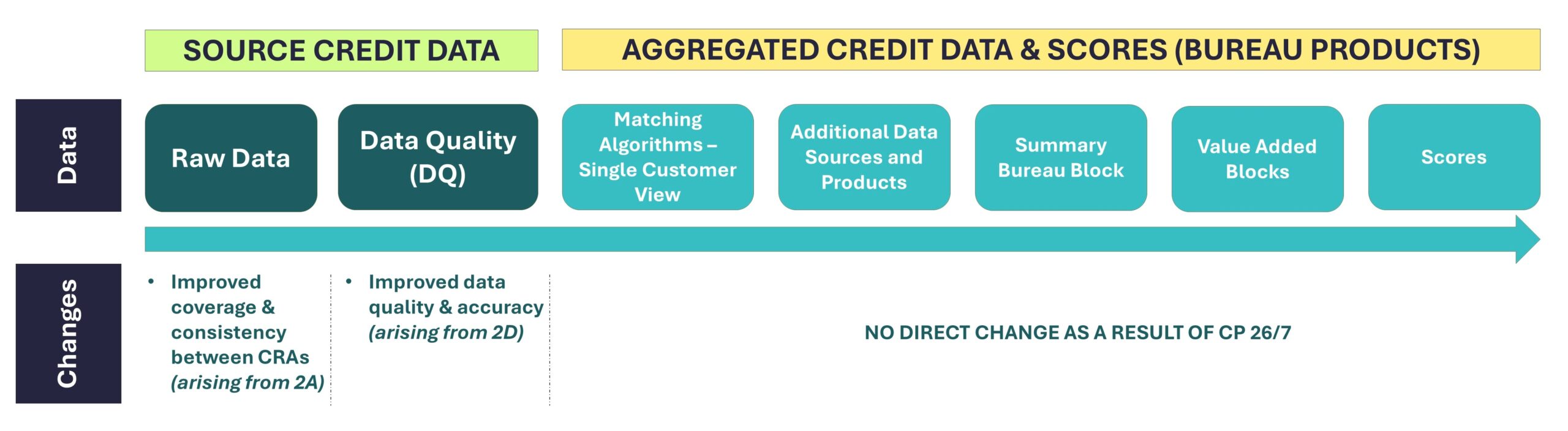

Figure 2: Credit data pipeline

Summary observations:

- The benefits of a multi-bureau approach are likely to be further diminished, with CRAs increasingly aligned in their core credit data.

- Firms may observe step-change in aggregated bureau reporting returns as previously absent lender data is introduced, and will need to understand the impact on their decisioning, capital & impairment models and remediate as necessary.

- While the FCA have highlighted mandatory sharing requirements will not encompass Current Account Turnover data, through the industry-led remedy 4C we are observing evidence that CRAs are now allowing firms without Current Accounts to access this data and therefore enhance their Affordability solutions with the additional information this provides.

- Firms should expect CRAs to continue to pivot their service offering – with a focus on the accuracy of their matching algorithms, unique additional data feeds, as well as novel aggregation and scoring techniques.

- Firms looking for an uplift in match rates do not need to wait for these changes and should consider evaluating the different bureau settings they have available, in our experience the settings drive a greater than expected difference

CP 26/7 represents a turning point for the UK’s credit information landscape. The changes will require significant investment in data governance, reporting technology, and customer facing processes for all firms that provide data to the CRAs.

Firms have until 1 May 2026 to engage with the consultation, but those who prepare early will be best positioned to transition smoothly into the new regulatory environment.

Get in touch

Send us an email if you would like to discuss this topic in more detail or explore ways 4most can support your organisation – info@4-most.co.uk.